Executive Summary

Climate change has become a central concern for investors. At Aberdeen Standard Investments (ASI), we have already made huge strides to enhance engagement with companies on climate risk, carbon-foot-printing portfolios and building tailored climate portfolio solutions. However, companies do not operate in a vacuum. They are affected by the political and policy environment in the countries in which they operate and generate revenues.

Our Social Capitalists index provided a first step towards understanding the environmental, social and political characteristics of different countries. The next step on our ESG journey is to assess the implications and opportunities arising from the low-carbon energy transition for investors. Our four step framework for analysing climate policy risk and opportunity provides investors with a process to incorporate macro factors into their investment strategies.

Step one identifies the structural energy endowment, economic, climate and demographic conditions that pre-dispose countries to specific climate mitigation challenges. Step two then assesses countries’ political backdrops to determine the main factors influencing environmental policy. With this knowledge in mind, in step three we evaluate environmental policy in terms of existing and proposed environmental initiatives. Finally, in step four we investigate the investment opportunity set, examining market structures and flagging risks associated with climate policy.

This can be seen as a checklist for investors to understand the climate policy risks they are exposed to via both micro and macro investment strategies. This can be used in the context of risk mitigation in traditional portfolios, opportunity assessment in devising green energy transition strategies and ongoing monitoring of country dedication to climate change in sovereign assessment.

The EU, China, India and the US are responsible for around 60% of total global CO2 emissions and so are crucial to mitigating climate change. We therefore use them as case studies for our evaluation framework. Unsurprisingly, the EU stands out as a leader, with strong political commitment to combating climate change backed up by robust market instruments, providing a relatively stable environment for investment. Nevertheless, further work to decarbonise the economy is necessary, providing opportunities for astute investors.

The United States case highlights how party politics can stymie the low-carbon energy transition. The country is deeply divided on the importance and causes of climate change. This is clearly visible in the roll-back of federal regulations mitigating climate change by the current Republican administration. It also makes 2020 a key election for investors trying to assess the opportunity set; if a Democratic candidate is elected to the presidency, federal environmental regulation is likely to become much more stringent, though congress will still operate as a constraining force.

In the meantime, most climate policy action is happening at the state level with California and the north eastern states leading the way in more stringent climate legislation. The upshot is that investors may be better off targeting state-specific opportunities, via municipal bonds, local infrastructure projects or region-exposed companies, which benefit from a more stable and supportive local political environment.

In China, air quality problems have highlighted the dangers of carbon-intensive growth, with the centralised Communist party-led system making it easier to align political imperatives with policy action to mitigate emissions. Indeed, the government’s pursuit of greener energy has led to them meeting their Paris 2020 commitments ahead of time. However, much more needs to be done and there is a danger that institutional commitments in China are weakened by economic pressures and a shift to quality rather than scale in renewables that needs careful policy management. For investors, transparency and market access are improving but from a low base.

India’s multi-party, federalist democracy contrasts sharply with China’s system, which alongside low voter interest means that climate policy action has been limited so far. However, air quality issues and severe weather risks may help to create more immediate pressure to act from companies that are affected. There are early signs that this is starting to happen. Incentives for renewable energy and an increasingly open market are creating new opportunities for investors, although issues of low transparency and weak enforcement of regulation remain acute.

These countries are just the first to be assessed within our framework, which will be rolled out to more countries and regions over time. Indeed, in providing this checklist for assessing climate policy risks and opportunities at the macro level, we aim to equip investors with the tools to build out more robust country-level analysis to match the substantial company research that already exists.

To ground the framework on a strong empirical basis, we also add to the limited country-level evidence base by building cross-country models that allows us to examine which factors are most strongly associated with economies’ carbon emissions and carbon intensity. Although emissions increase with a country’s population and per-capita GDP, higher living standards are also associated with greater carbon efficiency. Thus while economic development is a major contributor to climate change, it also points the way forward if governments can push through policy reforms like carbon pricing that catalyse greater zero-carbon energy use and innovation and decouple development from emissions.

As global policy action continues to ramp up and the relative price of low carbon energy technologies continues to fall, the implications for asset prices will be profound. The future will be bright for firms and countries that move quickly to respond to the changing landscape. Conversely, late movers will be left behind, particularly in carbon-intensive sectors of the global economy. These issues are explored in the complementary ASI white paper “Strategic Asset Allocation: ESG’s new frontier”.

Of course climate risk is about more than managing the energy transition. While massive policy change on a global scale is needed to address the climate challenge, government incentives are often skewed towards prioritising short-term economic and social challenges. And with multilateralism having been weakened by the surge in political populism, the policy coordination that is needed to overcome free-riding incentives is becoming harder to achieve.

The upshot is that current binding, policy-backed national commitments to reduce emissions fall well short of what is necessary to keep global warming relative to pre-industrial levels to below two degrees celsius. As a result, the physical risks arising from climate change, including significant costs of adaption in the worst-affected regions of the world, also loom large, particularly in the longer-term. The ASI white paper ‘Investing in a Changing Climate’ details these risks and the challenges they pose to investors.

The politics shaping the climate change outlook

In this video, Stephanie Kelly, Senior Political Analyst, explains why politics and climate issues are inextricably linked. By looking at the climate policy of individual countries, we can better appraise the financial effects of climate change on companies. And we can better gauge the likely success, or otherwise, of global efforts to tackle climate issues.

Authors

Stephanie Kelly

Nancy Hardie

Jeremy Lawson

Contributors

Rong Fu

CHAPTER 1

Global warming and climate change risk have become a key focus for policy makers an d investors alike in recent years. Global warming refers to the upward trend in average temperatures across the world, beginning in the early 20th century.

Warming has accelerated in recent decades as greenhouse gas emissions have grown more rapidly, with temperatures rising by 0.9 degrees since the early 1980s alone (see Chart 1).

For investors this research provides an innovative guide to considering climate change and transition prospects, complementing existing ESG investment capabilities at ASI

Chart 1: Things are heating up

Chart 2: More extreme events occurring

Greater awareness of these issues has been accompanied by major transnational government commitments to arrest the speed of global warming. The Paris Agreement within the United Nations Framework Convention on Climate Change (UNFCC) is the primary global agreement. The 195 signatories agreed to keep global temperature increases well below 2 degree Celsius above pre-industrial levels and to pursue efforts to limit the temperature increase to 1.5 degrees Celsius.

However, this agreement has been widely criticised because it has no enforcement mechanisms and, while some countries have embarked on policy change specifically in the name of the Paris agreement, many are failing to embed their commitments in tangible, meaningful legislative change. Indeed, research body Climate Action Tracker estimates that the maintenance of the current policy status quo would result in an estimated 3.3 degrees celsius warming above pre-industrial levels.

The main policy options for emissions mitigation include:

Limiting bad behaviour – regulations and limitations: National or local governments can impose regulatory limits or conditions on greenhouse gas emissions for companies and households in specific areas, such as emissions standards for energy production and cars, white goods and building standards.

Rewarding good behaviour – subsidies: National or local governments can provide financial support and incentives, such as subsidies, feed-in tariffs or tax relief for corporations and households that pursue more sustainable energy use.

Supporting innovation – R&D and technology support: Governments can provide support in the form of direct investment, tax breaks or subsidies to incentivise innovation in renewables.Supporting innovation – R&D and technology support: Governments can provide support in the form of direct investment, tax breaks or subsidies to incentivise innovation in renewables.

Setting a carbon price – emissions trading schemes and carbon taxes: For governments seeking to reduce emissions in an economically efficient way, pricing emissions forces firms and households to internalise the social cost of their actions without mandating how they achieve the necessary reductions. Emissions Trading Schemes cap the emissions of participating firms, allowing the price of carbon to fluctuate with the demand and supply for permits. Carbon taxes fix the level or path for the price of carbon, allowing actual emissions to fluctuate instead, though the tax should be calibrated to achieve specific climate goals.

Climate engineering - often referred to as geo engineering, this an umbrella term referring to direct technological responses to climate change such as removing carbon dioxide from the atmosphere or solar radiation management. The efficacy of such solutions has not been tested but they are sometimes seen as alternatives should the mitigation options outlined above fail.

Thus far, real world policy action has been underwhelming. The challenge of climate policy is applying policies that maximize pollution reduction while minimizing the long-term cost to firms, individuals and the broader economy. But uncertainty about the impact of different policy choices on the implicit carbon price prior to implementation, the fact that mitigation policies bring with them direct and indirect costs to voters in the short-term and political election cycles complicate this process.

Fortunately, the power to influence corporate behaviour is not the sole reserve of governments; investors can and are making waves mitigating climate change. While the investment community is highly exposed to climate change risks, it is also empowered to affect corporate behaviours to mitigate these risks at the source as a complement to government policy.

At ASI, we are engaging with companies on their governance and climate risk planning; building portfolios to encourage better behaviour or support clean energy providers. Additionally, we are building climate risk scenario analysis to illuminate the impact of climate change. This paper adds to this work, providing an additional lens for investors to understand climate risk by exploring the specific challenges facing different kinds of countries in mitigating climate change, focusing on the largest component of GHG emissions with the most data availability: CO2emissions (see Chart 3).

Chart 3: CO2 the main source of global emissions

While extant academic work has analysed the drivers of CO2 emissions, many studies tend to focus on single countries or small regional group comparisons. Global assessment and comparisons are therefore lacking. Additionally, discussion of effective, realistic policy options sometimes takes place independently of research into the deeper, fundamental drivers of countries’ emissions. This often leaves investors lacking a framework for understanding how different economic and political factors affect climate policy in different countries.

This paper addresses this vacuum in two ways. First, we model the challenges and opportunities for addressing climate change, based on the economic, climate and institutional factors associated with CO2 emissions in different countries. This exercise highlights that countries face differing initial constraints that crucially condition the potential for transition going forward.

We then use this information in our four-step framework for investors to assess climate-policy risk at the country level. This process involves identifying structural challenges, political risk factors, policy dynamics and investor opportunity. For investors, it provides an innovative guide to considering climate risk and transition prospects at the country level, complementing our extensive existing ESG investment capabilities at ASI. Specific applications include:

Risk assessment for investors: The framework provides a risk assessment tool regarding the operational environment affecting portfolio strategies, both in bottom-up fund management and in macro investing.

Opportunity assessment for bottom-up and top-down investors: For investors seeking to contribute to climate change mitigation, this framework provides the crucial questions for investors to understand where those opportunities are and how investors can benefit. It should be considered a “need to know” checklist before building a climate solution.

A comparative country scorecard: Our comparative heat-map, which uses the framework results to compare opportunities and challenges across country, provides a potential screen for investors as to the countries with the most relative opportunity to contribute to climate change.

Tracking portfolio exposure over time: The framework allows for investors to continue to sense check climate exposure on an ongoing basis, either for risk management or to ensure drivers remain in place for climate investment strategies. For further information on how to incorporate ESG factors into long-term decision making, see the recent white paper “Strategic Asset Allocation and the ESG factor”.

Building a model of global CO2 emissions intensity

CHAPTER 2

Broadly speaking, the empirical work on CO2 emissions focuses on identifying meaningful relationships between emissions and economic factors.

The Kaya identity is the principle equation for explaining CO2 emissions. It asserts that the level (and change) in emissions can be decomposed into four factors: population size, GDP per capita, energy intensity and carbon intensity per unit of energy consumed (see Table 1).

Table 1: Kaya identity for major emitters

However, the Kaya identity is only the starting point for understanding the drivers of carbon dioxide emissions. It does not explain 100% of CO2 emission variation at the global level and is not granular enough for targeted policy analysis. For example, energy intensity and carbon intensity themselves are a result of specific economic, political and environmental factors. Understanding these factors is crucial to understanding the space for policy and investment.

The broader econometric analysis in the academic literature suggests a wide array of more specific factors that affect CO2 and greenhouse gas emissions beyond the Kaya identity. Trade openness, Foreign Direct Investment (FDI), an economy’s industrial structure and of course its energy mix, have all been identified as being important drivers at the country level.

However, this empirical literature is itself far from complete. Studies often use different modelling techniques, make different choices about which countries and regions to include in the study and suffer from omitted variable bias by not including sufficient information about policy factors, such as carbon pricing regimes, or non-policy factors, such as countries’ basic climate typology or population density, that may influence emissions and emissions intensity.

Measuring association on a global scale

We have addressed some of these deficiencies by building a global cross-country random effects model for 105 countries that associatively explains CO2 emissions and CO2 emissions intensity as a function of 14 economic, political and environmental variables gathered between 2002 and 2014 (please contact authors for technical appendix). Data constraints prevented more countries and years of data being included in the analysis.

We chose independent variables from six key categories potentially relevant to CO2 emissions and emissions intensity (note that data limitations prevent us from including a range of other potentially important variables):

Economic Development – GDP per capita is used to capture the relationship between the level of economic development and both emissions and emissions intensity, while the square of GDP per capita is also included to identify any non-linearities in the relationship. Industry’s share of total value-add is included to determine whether an economy’s structure influences emissions, given the sector’s concentrated use of fossil fuels.

Demographics – Population size is a key component of the Kaya identity as a country’s level of emissions will naturally rise with more people and it may also influence emissions intensity. Population density is included because the dispersion of a country’s population can influence transport and energy infrastructure decisions, as well as patterns of energy use.

Energy mix – A country’s energy mix will obviously affect its emissions and emissions intensity. We focus on country’s renewable energy share and mainly use it as a control variable to help identify the influence of other variables in the model.

Climate related policy – Policies to price carbon formally, either in the form of an ETS or a carbon tax, are designed to influence emissions and emissions intensity. Decisions to price carbon may also reflect broader commitments to constrain emissions. To separate announcement from implementation effects we construct dummy variables identifying when countries have announced but not yet implemented ETS or carbon tax, and then when implementation has occurred.

Climate – A country’s climate itself will influence its energy-use patterns. For example, countries with tropical climates will make less use of centralised heating than countries with very cold winters. While the climate type is not amenable to policy change, including it in the model helps us understand the nature of each country’s mitigation and adaptation challenges. We construct dummy variables for five Koeppen-Geiger climate categories - mild-humid, desert, highland, snowy-forest, and tropical based – based on which climate type the largest proportion of the population is living in.

Politics and governance – Stable, transparent and open political institutions have been found to improve the quality of policy formation, so we included the Political and Governance Sub-index used in our Social Capitalist research to capture the potential effects on emissions via climate policy in the model (see Chart 4).

Chart 4: ASI ESG Politics and Governance Sub-Index

Innovation – Environmental research and development can directly influence countries’ emissions, or simply reflect a broader commitment to mitigation. We therefore include a variable that measures environment-related patent applications as a proportion of total patents.

In addition to the model that includes all countries, we also ran separate models for high income, middle income and low income countries as another way of isolating and controlling for the development effects that dominate the dispersion of emission and emissions intensity across countries.

The table below illustrates the results of the CO2 intensity models (please contact authors for technical appendix) showing the sign, magnitude and statistical significance of each variable’s relationship with emissions intensity within our sample.

Table 2: Global CO2 emissions intensity model results

Results

CHAPTER 3

Before discussing our results in more detail, it is important to add a note of caution. Omitted variable bias due to data constraints, as well as explanatory variables that are co-determined and are themselves likely to be influenced by emissions, means that our model does not identify causal relationships.

Instead, it should be thought of as a collection of associative relationships, indicating the directionality and broad magnitude of how each indicator varies with emissions intensity.

Economic development matters but it is not the whole picture

These caveats notwithstanding, we are able to identify a number of plausible and interesting relationships. The strongest relationship in both types of model is unsurprisingly with per capita GDP. In the CO2 emissions model, the relationship is positive, showing that emissions tend to rise as countries become wealthier. This mainly reflects the fact that total energy use is higher among more developed countries, and fossil fuels still dominate the energy mix in most countries.

However, while total emissions rise with development, the emissions intensity of economies is negatively associated with per capita GDP. Although this implies that energy efficiency and intensity both tend to decline as countries develop economically, it is far from the whole picture. For example, most of the explanatory power of economic development on emissions intensity comes from the variation across the three per capita income groups in the model. This is reflected in the fact that the coefficients on the per capita GDP variable are much smaller and in the case of low-income countries, statistically insignificant.

While the result likely partly reflect the fact that, by definition, a lot of the variation in per capita GDP occurs across the income groupings, it is not a full explanation because per capita incomes still vary significantly within the categories. For example, the US has much higher per capita GDP than the EU average, yet emissions and energy intensity are both higher. The same holds for the comparison between China and India.

So, what else is going on here? We think it shows that the relationship between prosperity, energy efficiency and environmental goals is far from deterministic, with substantial space for national preferences and policy choices to influence outcomes.

A role for industrial structure and the energy mix, but not our measure of innovation, yet…

Unsurprisingly, industrial activity as a percentage of a country’s GDP has a positive, significant relationship with carbon emissions intensity. This simply reflects the energy-intensive nature of existing manufacturing and allied production, as well, of course, as the continued reliance on fossil fuels. On the flip side, countries where renewable energy is more important in the overall energy mix have lower emissions and emissions intensity.

In contrast, our measure of environmental innovation did not have a statistically significant relationship with emissions or emissions intensity, except for in the lowest income countries. The general result is probably explained by the relatively nascent stage of the climate technology cycle, and its diffusion. It may also capture the fact that patents can affect technology choices outside of the countries in which the patents are first applied. For low-income countries, where patent activity is generally very low, the result probably says more about environmental objectives having more weight in select countries than the direct effects of innovation itself.

Pollution halos, personal space and the benefits of warmer climes

While a country’s population size has a strong influence on its total emissions, in line with what we would expect from the Kaya identity, it does not influence emission intensity — in our modelling at least. On the other hand, population density is significantly negatively associated with emissions intensity. This likely reflects the fact that mass public transportation is more economical than single driver cars (see Chart 5) and likely to develop in more densely populated cities and countries. A caveat is that it is harder to apply this result to countries with low average population density, resulting from large uninhabited spaces like Australia and the African countries touching the Sahara.

Chart 5: Mass transit emits less CO2 per km

Although it is common to include FDI stocks or flows as an explanatory variable in emissions models, estimated effects are not very precise and depend heavily on which countries are included in the sample as well as other modelling choices. Though we find evidence of a negative relationship between FDI stocks and emissions intensity – consistent with the existence of pollution halos, whereby FDI inflows improve energy efficiency through better use of technologies and management practices – the effects are generally quite small.

In a departure from the wider literature, we also incorporated climate variables themselves to understand how a country’s long-term weather patterns are associated with CO2 intensity. Relative to mild-humid climates (the base case in our model), the most robust result was that countries with a majority of their population living in tropical, desert or highland climates tended to have lower CO2 emissions intensity, likely reflecting a reduced need for fossil-fuel intensive temperature control.

The importance of carbon pricing

Concrete action to reduce carbon emissions, particularly in a way that raises energy prices, weighs on employment in fossil-fuel intensive industries, or is seen to inhibit economic development, is politically contentious in many countries. This helps explain why few countries are taking large enough steps to limit climate change despite the environmental imperative.

Nevertheless, in those countries that have pressed ahead with at least some sort of carbon pricing regime, emission intensity is lower than in other countries holding all else constant. Interestingly, that holds whether carbon pricing has merely been announced or fully implemented. The presence of announcement effects suggest that while carbon pricing itself is likely playing some role in constraining emissions, the variable likely also picks up the fact that countries prepared to price carbon have a stronger broader commitment to limit climate change. Regardless, these countries are a great place to start for those looking for climate champions (see Chart 6).

Chart 6: Carbon pricing across the world

*NOTE: AUSTRALIA’S SYSTEM IS INCLUDED BY THE WORLD BANK BUT IS ACTUALLY AN EMISSIONS REDUCTION FUND (ERF) RATHER THAN AN EXPLICIT ETS OR CARBON TAX.

SOURCE: WORLD BANK (AS OF 2019)

Our measure of the quality of countries’ political institutions is not robustly associated with emissions or emissions intensity. Though this result could be taken at face value, it may also reflect the fact that the institutional quality most relevant for policy in this area is being picked up by other variables in the model such as the carbon pricing indictor.

Our model is better at predicting CO2 intensity in some countries than in others

Our model produces a benchmark CO2 emissions intensity estimate based on the statistically significant variables included in the model. A comparison of actual CO2 emissions intensity against the benchmark estimate implies that the model performs relatively well in sample. In 65 countries estimated intensity is within 10 basis points of actual intensity, though intensity is slightly more likely to be overestimated and there are 35 countries for which the error is greater than 10 basis points (see Chart 7).

The adjusted R2 of the models, which range from 0.4 to 0.56, is also reasonable for a model drawing primarily on cross-sectional variation, though it is also indicative that important explanatory information is missing. This is not surprising given that many of the factors that influence the structure of the economy, the energy sector as well as policy choices, and hence emissions intensity, cannot be measured in a consistent way across countries and over a long enough period of time.

Looking more closely at the countries for which the model’s errors are largest, some interesting patterns emerge. One is that the model overestimates emissions intensity in many North African countries, with Morocco, Algeria, Tunisia and Niger making up four of the top five most overestimated countries. These errors may be related to the fact that the Sahara desert makes up a large share of the total land mass but only a small share of where the population lives.

Chart 7: Residuals show variation in model’s predictive ability

Finding the champions for climate change: a framework for investors

CHAPTER 4

Our experience of modelling CO2 emissions intensity illustrates the complexity of the factors at play. Climate change, energy transition and the associated policy issues are challenging for investors to come to grips, but with potentially profound implications for investment outcomes and opportunities, as well as portfolio construction.

Table 3: Climate change policy risks and opportunities framework

We can complement this work with a systematic assessment of the country-level characteristics and policy outlook that will shape the investment opportunity set over the coming decade. Our proprietary framework provides a guide to finding the Climate Change Champions. These are the countries:

that are acting now to mitigate climate change;

where support for further action is deep and broad enough to make us confident that policy will remain supportive over the longer term: and

where market structures allow investors to access the emerging opportunities.

For macro investors, the framework provides a more systematic way to identify national opportunities, risks and constraints when considering investment strategies that take climate change into account. For bottom-up investors, our framework facilitates a greater understanding of the national economic, political, policy and market factors that companies are operating within.

Step 1: Country Characteristics

Our CO2 emissions intensity model illustrates how individual country characteristics are associated with different emissions profiles. By understanding population density, economic structure, energy endowment and prevailing climate and physical risks, we can establish a baseline for carbon emissions as well as emissions intensity, and thus a more nuanced understanding of the scale of the mitigation and adaptation challenge each country is currently facing (In-depth discussion of physical risks can be found in the ASI White Paper: Investing in a Changing Climate).

Step 2: Political Backdrop

Once we understand a country’s characteristics, investors need to identify the political dynamics influencing the policy environment. Policy promises are only as strong as the political commitments underlying them. The more closely aligned political parties and other key stakeholders are on climate change policy, the more consistent and thus predictable the policy environment.

In the US, for example, the Republican and Democratic parties are deeply divided on the importance and appropriate policy solutions for climate change (see Chart 8). This makes finding a majority for policy difficult to legislate efficiently and effectively. It also increases the chances that policies are changed or reversed on short time scales. That in turn increases uncertainty about the return on long-term investments, raising the hurdle rate on projects.

Chart 8: Climate change third most important issues for Liberal Democrats but 29th for Conservative Republicans

SOURCE: EUROBAROMETER, ASIRI (AS OF 2019)

The nature of a country’s political institutions is also fundamental to assessing the potential for action on climate change. The more stable and transparent the political institutions, the greater visibility investors can have of the political agenda. Investors can understand this environment better by using the political and governance scores in the ASI global ESG index. This ranks countries by their political stability, institutional transparency and political freedom.

Meanwhile, constitutional arrangements are also important. In federal systems, for example, the powers to determine and influence climate and energy policy are usually shared between central, state (provincial or regional), and local government authorities. This raises coordination challenges, particularly when climate mitigation is contested politically, while making it more important for investors to consider the location of potential investments within a country. The US is a prime example of this; while climate policy has stalled at the federal level, progress is being made in Democrat-dominated ‘blue’ states.

Step 3: Policy Action

Following the assessment of the politics of climate change in a given country, investors should assess the concrete climate policy agenda. Many countries have signed up to the Paris climate agreement. However, in the absence of explicit legally-binding enforcement, the prospect of genuine policy-induced change should be treated with scepticism unless backed up by strong domestic policy actions. Climate Action Tracker has flagged that even existing policy agreements are insufficient to prevent warming beyond the two-degree goal (see Chart 10).

Chart 10: Many existing commitments are not enough

SOURCE: CLIMATE ACTION TRACKER (AS OF 2019)

Legally-binding commitments, such as regulatory quotas on emissions for particular sectors like the stationary energy sector, create both a short-term risk for companies specifically affected and longer term opportunity for climate change fund investors.

Some countries go a step further, embedding environmental policy into all policy decisions, so that for all policy decisions in health, education, transport etc. there is an awareness of the climate impact. We consider this approach a positive signal regarding the extent to which climate policy is considered a long term issue rather than a short term political strategy.

The decision to explicitly price carbon, by implementing a carbon tax or emission trading system (ETS), has potentially profound implications for corporate earnings and sector trends. However, it is also a signal of government commitment to the energy transition. It creates an opportunity for investors seeking to invest in countries based on their environmental commitments, e.g. ethical funds.

Carbon pricing regimes have the advantage of being a market mechanism that helps ensure that climate change mitigation and greenhouse gas abatement occur at the lowest possible cost to the economy. However, where carbon pricing is in place, investors should also understand the implied level of the price and how widely the price is applied. A narrow ETS affecting only one industry or sub-industry with generous allowances or a tokenistic carbon tax may struggle to move the dial on climate change.

Meanwhile, most countries whether formal carbon pricing is in place or not, have an array of policies in place that embed an implicit cost of carbon abatement. Renewable energy targets, energy efficiency standards for goods and buildings, all fit within this policy category. They usually have an implied abatement cost well above what would exist in a carbon pricing regime. When assessing opportunity sets, investors need to understand these policies, how they interact, and how they influence and potentially distort investment returns.

Policymaking is also more effective when it does not take place in a vacuum. It is important that climate policy targets the sectors contributing most to CO2 emissions and intensity, and that government engages with business to design policy solutions that smooth the transition path and take account of the nuances of business operations. For countries that face substantial physical risks of flooding, forest fires and extreme weather, policy should target these issues as a key part of the agenda.

Finally, though much of the climate policy discussion focuses on limiting behaviours that involve explicit or implicit costs, many policies are designed to incentivise ‘good’ behaviours through measures like tax credits, subsidies and feed-in tariffs. Understanding how these influence the return on different investments and alter behaviours is critical for forecasting earnings in affected companies and sectors. It is also critical for gauging the extent to which governments are succeeding in encouraging good behaviour. Of course, even though such policies are presented as incentives rather than punishments, they also have opportunity costs and implicit abatement costs.

Step 4: Investor Opportunity

The final step is to assess investor opportunities in the market under consideration. This is particularly applicable for investors seeking to increase asset allocation to countries with greater climate change mitigation potential. This step allows investors to determine the ways to tap into markets with potential, or indeed highlights the barriers that remain.

Insurance firms, businesses reliant on agriculture and water and real estate are particularly exposed to physical risk. We cover this in depth in our Investing in a Changing Climate paper. Investors should assess how these sectors are changing, how consistent that this is with the trajectory for policy, and whether there is an opportunity to support that change.

Investors should try to identify the climate change winners in those key sectors. These may be firms that are actively engaging with government, or are moving to renewable solutions as a result of - or indeed in spite of - government policy action.

Scoring countries on their transition prospects

The framework provides not only single country analysis (see case studies below) but a systematic approach that can be adapted for cross-country comparison. For investors looking to assess multiple countries for opportunities to contribute, we have built out a heat map extension to visualise the opportunities and challenges across countries.

This heat map ranks countries for each of the assessment categories; country characteristics, political factors, the policy backdrop and market opportunities. On a sliding scale from green to orange to yellow to red, the heat map provides an instant visual of the relative strengths and weaknesses in each country.

For data we can quantify, like economic structure or climate, this is based on how each country performs in terms of quartiles of the overall global dataset. For data that requires qualitative analysis, like politics and policy, we built out a four-tiered descriptive assessment. This is more subjective than the quantitative quartile approach, reflecting the fact that climate policy and politics is complex and subject to interpretation (please contact authors for technical appendix).

Indicative numerical scoring is then applied based on the colour of each indicator. Green is given a value of three; yellow is given a value of two; orange is assigned one point; and red gets a score of zero. These scores can then be added up to provide an indication of overall transition preparedness. However, the distribution of the scores is important too; for example, a favourable political environment is of little use if investors cannot access opportunities in the market due to liquidity constraints. Similarly, an open market with a problematic political backdrop makes long term investing in the transition more challenging.

Chart 11: Heatmap visual

Comparing the major emitters

Plugging the US, EU, India and China into this heat map provides an opportunity to compare the relative climate transition opportunities and challenges. The EU is clearly the region with most commitment and opportunity to engage on climate transition, with an open market and extensive political momentum following recent European elections.

Chart 12: EU surpasses other major markets on climate policy opportunity

The US, on the other hand, has strong partisan divisions on climate change. So the party in power determines the prospect for binding national regulation. However, environmental policy is much more activist in Democrat-led ‘blue’ states and cities, creating an uneven policy environment across states. As a result, investors need to focus on activist corporates and states to find transition opportunities and physical risks.

Physical risk is a real and present issue for China and India, where reliance on coal is contributing to both countries’ infamous air pollution problems and weaker performance in our heat map. However, China contrasts sharply to India in this respect: its Communist party-led system has been more actively driving a green mandate over the past decade. Slowing economic growth has stymied progress more recently, reducing the strength of its policy component in the heat map.

India contrasts with China’s single party system as multi-party politics and little interest from voters means that climate change policy has been limited. Growing policy incentives for renewable energy and an increasingly open market are creating opportunities for investors. However, investors should bear in mind that transparency and regulation still have much room for improvement in the burgeoning renewables market.

Conclusions

As investors, we have a responsibility to understand the depth of the climate challenge and how that will affect sectors, as outlined in the white papers “Investing in a Changing Climate” and “Strategic Asset Allocation and the ESG factor”. All four regions in our comparative assessment present opportunities for investors to lead on climate change. However, the pre-conditions in these regions, their politics and policy are all different. This will determine the opportunity set for investment.

Our global model of CO2 emissions intensity underscores key messages to this effect. While our analysis found that characteristics like climate and population density have important associations with CO2 emissions intensity, the results also suggest that there is a really significant role for policy to act to mitigate climate challenges. The ongoing link between GDP growth and total CO2 emissions remains clear in our modelling.

This reflects the extent to which growth is still reliant on fossil fuels, even in top-performing regions like the EU. Breaking this link will not be easy and creates huge policy challenges for all economies. For example, large emerging markets like India face the challenge of sustaining substantial growth to lift their populations out of poverty in a more sustainable way. This highlights the need for global coordinated solutions to the climate challenge to smooth the transition across the global economy and minimise any unintended consequences on particular countries and people. However, the current political environment of sovereign politics and populist forces makes cross-border progress really difficult to see in the short term.

These huge macro questions about the outlook for policy, coordination and transition underscore the need for investors to understand the politics and policy of climate change. Doing this allows investors to better understand the challenges posed and solutions found by different countries to address climate change in the face of economic challenges, social unrest and corporate interests. The US illustrates clearly how polarised party politics can impair the policy environment. China highlights how even substantial progress leaves much work to do in countries with large reserves of fossil fuels facing economic constraints.

Much of the opportunity for investors to contribute to transition or physical risk reduction requires a nuanced understanding of these dynamics. The framework outlined in this paper provides a structured process and checklist for investors to ask the right questions based on rigorous empirical analysis and in-depth policy research. We illustrate how to use them in the case studies attached for the US, EU, China and India. However, they can be applied similarly to all countries to investigate climate opportunities and risks. Armed with that understanding, active managers have the opportunity to find value and returns for clients, both in financial and environmental terms.

Deep dive into regional challenges

CHAPTER 5

Our Climate Champions framework can be applied to any country to build indepth understanding of the policy environment. Applying it to the United States, China, India and Europe illustrates how to use it to find investment opportunities and identify risk.

Case Study 1: United States Climate Policy Risk Assessment

The US is heavily reliant on fossil fuels, particularly in low population density, industry-intensive colder states

The United States is the second largest generator of CO2 emissions in the world, second only to China, accounting for 15% of global emissions in 20171. It also ranks 102nd of 135 for carbon intensity in our global ESG index as a result of its high reliance on petroleum and coal (see Chart 13).

A novel way of showing this is to compare trend growth with the standard deviation of growth. Our estimate of Eurozone trend growth is a lowly 1.3% per annum, declining to 1.0% over the coming years. However, the 15-year rolling standard deviation of growth is 2.5% (see Chart 1).

Chart 13: Fossil fuels dominate US energy mix

Low population density, widely dispersed population centres and comparatively low fuel taxes have all limited the development of mass public transportation. Alongside an almost complete dependence on petroleum, this has left the US transportation sector as the largest contributor to total emissions, despite being only the second largest user of energy (see Chart 14). In contrast, the stationary energy sector, which accounts for the largest share of total energy use, is only the third largest contributor to total emissions, mainly because non-fossil fuels, and ‘cleaner’ natural gas in particular, have made larger inroads into electricity production.

Chart 14: US Primary energy consumption by source and sector

Given low population density in some areas, companies developing battery storage in renewables present an opportunity for investors. Given the search for efficient and cost-effective storage options and scope for development in wind energy, investment in transmission to deliver renewable energy to where end users are located may provide the next front for renewables in the US.

At the state level, CO2 emissions intensity can vary significantly depending on climate, population density and energy endowments. States with relatively high energy intensities tend to be in cold climates, rural areas or have a large coal or commodity-reliant industrial bases relative to their overall economy. These states include West Virginia, Wyoming, North Dakota, Alabama and Montana.

Meanwhile, states with low industry and electricity production alongside more temperate weather and higher population density, like California, New York and Connecticut, show the lowest energy intensity. This reinforces the messages from our global model that these characteristics play a crucial role in setting the baseline for emissions. State level variation is exacerbated by deep polarisation of voters on climate change in terms of whether climate change is real and how to address it.

Polarised climate politics and the four year election cycle create uncertainty for investors at the national level

Chart 15: Voter views reflect party preferences on climate

Although the US ranks highly in terms of the quality of its institutions in our global ESG index, key features of its politics and political system raise significant barriers to large-scale, durable and efficient action to address climate change. The US has the deepest, most liquid public financial markets in the world, as well as the most extensive private investment universe. So, the US has the market structure with ample space for investors to catalyse opportunities to support the transition; it is the politics that creates disincentives for investors in this space.

Environmental legislation is set by a deeply divided Congress and usually requires approval from the President, who also has executive powers to act unilaterally in regulating environmental policy. Democratic voters are much more likely to cite climate change as a key issue than Republicans (see Chart 15). Unsurprisingly, this is reflected in party politics locally and nationally. Indeed, many Republican voters and politicians reject the thesis that human activity is responsible for climate change altogether.

The US is a signatory to the Paris Agreement, targeting a 26-28% reduction in greenhouse gas (GHG) emissions between from 2005 levels by 2025. However, Climate Action Tracker estimates that current action is not sufficient for the US to reach this target. The US is even further behind the eight-ball when it comes to taking its share of the action necessary to limit global warming relative to pre-industrial levels to two degrees Celsius or less.

At the federal level, US climate policy tends to be implemented through regulation rather than binding carbon pricing – anchored on two key pieces of legislation:

The Clean Air Act regulates air emissions in the US from stationary and mobile sources. The Environmental Protection Agency is the key regulator. It is responsible for establishing National Air Quality Standards (NAAQS) and directing states to develop state implementation plans, new source performance standards and national emissions standards for hazardous air pollution (NESHAPS), acid deposition and ozone protection. This is done using technology and performance standards, maximum atmospheric concentrations limits and emission trading.

The Energy Policy Act and Energy Independence and Security Act set appliance, equipment and building sector emissions standards.

While these policies have been in place for years, the interpretation of regulation and willingness to further strengthen these commitments is heavily influenced by who holds Presidential office, who they appoint to the main regulatory roles, and the composition of Congress. The Obama administration’s initiative to strengthen climate change commitments with more stringent, wider scope motor vehicle and electricity sector regulation were limited by partisan politics and ultimately reversed by the Trump administration.

While incentive schemes do exist and help support solar and wind power, the scale of this support is limited and includes support for fossil fuels. The Congressional Budget Office estimated that in 2016 $11bn in energy-related tax preferences went to renewable energy, $2.7bn to energy efficiency and electricity transmission and $4.6bn to supporting fossil fuels.

At the national level, if President Trump remains in office following the 2020 election, we expect a continued reneging on climate commitments. If, on the other hand, a Democratic candidate is elected, we expect significant strengthening of the enforcement of climate change regulations.

However, the bipartisan dynamics in Congress make nationwide climate legislation highly unlikely whoever the President is. Importantly, the oscillation in policy every four years depending on the party in power creates problems for investors because there is insufficient predictability over the period in which an investment needs to pay off.

State and regional emissions trading schemes are promising, but to really have an impact on CO2 emissions, sector coverage should be expanded and carbon prices elevated

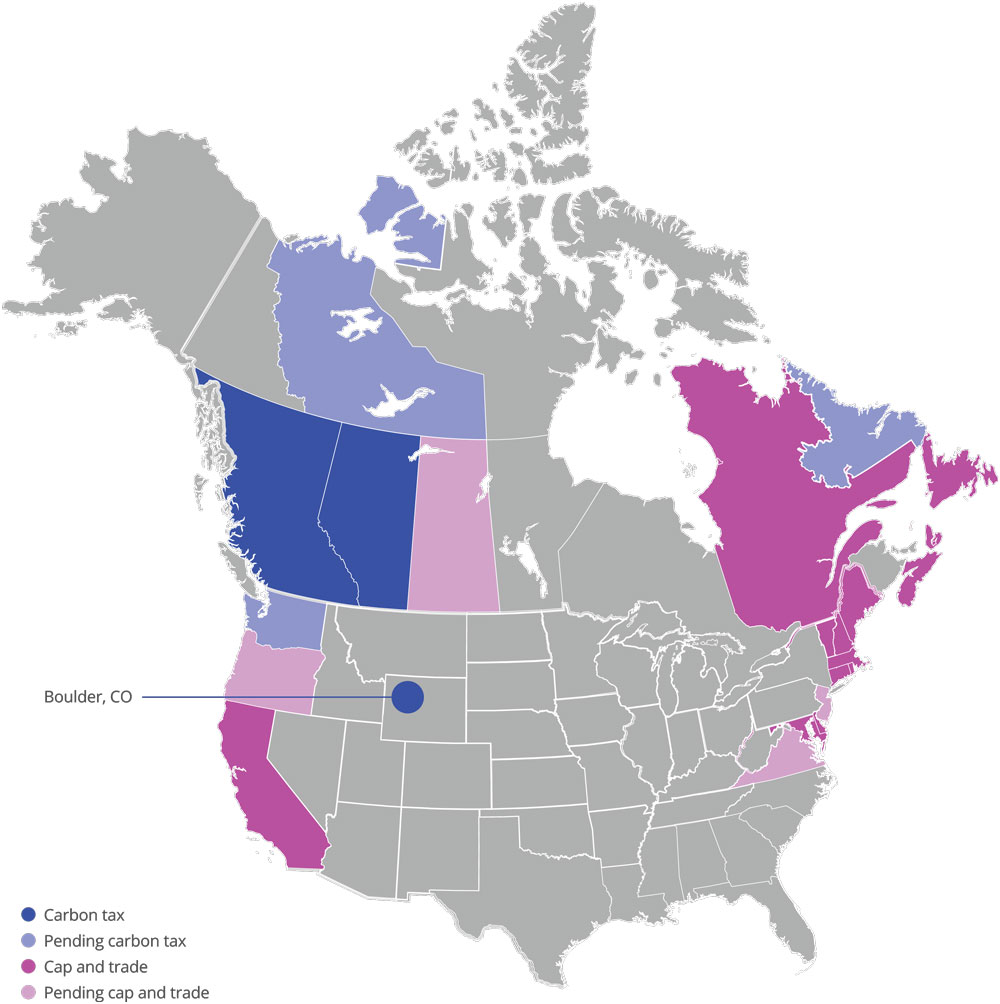

A partial counterweight to this pessimistic outlook for federal policy support is that significant power to regulated energy and the environment rests with states and local authorities. There are more signs of progress here: the US Climate Alliance is a bipartisan group of 25 states that have joined to commit to investing in the proliferation of green policies and emissions reduction. However, Democratic states tend to be much more active than Republican-dominated states, while control of legislatures fluctuates less than at the federal level.

The upshot is that states like California, New York, Massachusetts and New Jersey that have passed substantial legislation targeting emissions are less subject to short-term electoral politicking. These states present a more stable medium-term outlook for investors who can access opportunities in these states.

Chart 16: States lead the way on carbon pricing

*THIS MAP ALSO HIGHLIGHTS CANADIAN STATES THAT IMPLEMENT CARBON PRICING POLICIES

SOURCE: ACEE (AS OF 2019)

A good example of state-led progress is the Regional Greenhouse Gas Initiative (RGGI) - an emissions trading scheme that requires fossil fuel power plants with capacity greater than 25 megawatts to use allowances for CO2 emissions (see Chart 16). Connecticut, Delaware, Maine, New Hampshire, New Jersey, New York, Maryland, Massachusetts, and Rhode Island are all signatories to the scheme. However, the narrow sector exposure means that CO2 emissions affected only account for an estimated 1.4% of all US CO2 emissions.

California also has a much broader reaching cap-and-trade programme. This sets a statewide limit on regulated entities, which include electric power plants, electricity imports, large industrial plants, and distributors of transportation fuels and natural gas. The programme covers about 200 emitters, responsible for 80% of the state’s GHG emissions. This, together with the enormous size of California’s economy, means the programme covers approximately 5-6% of total US emissions. However, the implied price of carbon is still quite low in this programme, at an estimated $14.91 average price for allowances in 2018.

Investors increasingly have the opportunity to invest directly in the states and localities that implement climate action through municipal bonds. Cities, states, and agencies use municipal bonds to finance many of their infrastructure needs, and this increasingly includes responding to and preparing for the effects of climate change. Climate considerations affect municipalities’ borrowing costs and the pricing of their bonds, as rating agencies are moving towards more robust examinations of climate change response plans and greater incorporation of climate change vulnerability into ratings2.

The majority of green bond issuance is concentrated in issuers located in coastal states, notably California and New York, and in water- and transportation-related projects. This probably reflects from political and popular support for clean projects in these largely Democratic states. The ASI municipal investment team believes that considering a municipality’s exposure to climate risk along with the strength of its response plan can lead to long-term outperformance.

Even at the sector level, understanding state level dynamics is key for investors

At the sector level, state level regulation is more important for utilities than federal regulations. Investor-owned utilities are regulated by the state so the environment tends to be relatively stable, with regulators working with them to ensure smooth transition and relative earnings stability, e.g. ensuring gradual depreciation of assets.

Renewable energy infrastructure investment projects benefit from tax breaks. However, the state-level regulatory structure means that incentives for transition vary hugely if a company is in California, where renewable demand is high, or Kentucky, which remains highly reliant on coal consumption.

Large blue chip firms, particularly those in the technology and energy sectors, have played a key public role pushing for greater renewables penetration, e.g. via renewable power purchase agreements with suppliers. There are three campaigns being led by corporates pushing for formal carbon pricing at the federal level. These include: Americans for Carbon Dividends; a lobbying push via the nonprofit Ceres; and CEO Climate Dialogue, a group of large corporates and environmental groups. However, until climate change is recognised as a key issue in both major parties and voters, long-term stable policy solutions will be absent.

Growing pains and poverty make fossil fuels the easy option in India but declining solar prices are encouraging

Chart 17: Coal dominates the energy mix

India’s country characteristics strongly influence its carbon emissions intensity. It should not come as a surprise that the air-conditioning market is set to boom in the coming decade given tropical India’s growing middle class and higher living standards. Monsoon rains are increasing due to ocean warming, while damaging floods are becoming more common.

Despite almost 70% of its population living in rural areas, pollution is high due to the burning of crop stubble and use of biomass for heating and cooking. This prompted Modi’s government in 2016 to enact a scheme that supplies gas, a much cleaner fuel, to these rural households. However, cost and the long wait for refills has deterred use.

In 2014, 73% of India’s energy consumption was from fossil fuels. India has some of the largest coal reserves in the world and this is the primary resource for producing its electricity. India is unable to exploit these large reserves, due to the technical difficulty in accessing these resources as well as issues of land availability and environmental clearances. Accordingly, domestic coal does not satisfy the growing energy demand and this makes India reliant on fossil fuel imports. Similarly, despite its large oil and gas endowment, India imported 82% of its oil in 2018.

Given this mix, the energy sector dominates the country’s total emissions. Between 1990 and 2014, the use of coal increased more than proportionately to total energy demand, and 69% of total emissions now come from the energy sector. The most energy intensive industries in India are steel, iron, and cement, with coal their dominant source of energy. The cement industry is also one of the largest sources of emissions and production is predicted to triple in the coming decade.

Air pollution and forestry are two major environmental issues in India. Extreme heat, changing rainfall patterns, and drought are some of the physical symptoms of climate change that are already affecting India. Drought, for example, will affect basic needs and thermal power generation, and has already affected the agricultural sector.

However, there is some good news. Solar and wind power has become more price competitive, resulting in the removal of private capital from coal projects. Following the winding down of subsidies in China, India was one of the major growth centres for solar power in the first half of 2019. Encouragingly, tariffs on solar and wind have dropped to record lows.

Climate change is becoming more politically important and renewable energy support has risen, but both from extremely low bases given India’s economic challenges and historic reliance on coal

The elections just passed were the first in which climate change was presented in the manifestos of the Bharatiya Janata Party (BJP) and the Indian National Congress (INC). Both the BJP and INC’s policies focus on the need to significantly change India’s infrastructure in terms of its heavy reliance on burning fossil fuels. That said, climate change remains a low priority for voters. Job opportunities, water availability, and subsidies for farmers were issues that drove the rural areas (where the vast majority of the voting population lives) to the polls earlier this year.

Since Modi’s rise to power in 2014, India has announced several climate change targets, which so far have had some positive results. Green energy capacity has more than doubled since 2014, from 32 to 79GW, thanks to historically cheap prices. India is also increasing its use of nuclear energy and is set to rise to 22,480 MW by 2031. Meanwhile, subsidies for renewables increased from $431m to $1.6 billion between 2014 and 2016.

Chart 18: Energy mix projections

To help meet its goal of 100GW of solar energy capacity by 2022, the Ministry of New and Renewable Energy is providing subsidies to businesses that add to this capacity (see Chart 18). Wind power creation also receives financial and tax incentives for its contribution to the grid and is expected to contribute 60GW by 2022. In June this year, the Ministry of New and Renewable Energy asked for public sector banks to increase access to finance for renewable energy projects. DISCOMs, electricity distribution companies, are the renewables sector’s biggest customers due to long-term power purchase agreements at prearranged tariffs.

Chart 19: Renewable Energy Targets for 2022

Encouragingly, the recently amended Electricity Act now permits 100% foreign direct investments in renewable energy projects. The Renewable Purchase Obligations (RPO) require power distribution companies to source a fixed amount (dependent on the state) of their energy from renewables. Renewables must also comprise a tenth of power production from new coal and lignite capacity additions.

In July this year, a scheme was announced to engage with global companies using a bidding system to establish plants that produce solar cells, solar electric charging infrastructure, and lithium storage batteries. Between 2014 and 2016, tax and financial incentives for the solar and wind industries helped attract USD$2.05 billion to the renewables sector. However, the renewables market is poorly regulated and this makes the products less attractive for investment.

Ongoing coal reliance and a lack of binding, transparent policy enforcement means India’s more ambitious climate policy goals don’t have a clear path to success.

Despite India’s ambitious climate targets, the government spends roughly USD$25 billion on fuel subsidies per year to extend its fuel availability to the poor. Moreover, in 2017, the coal industry received three times more investment from state-funded financial institutions and banks than the renewables sector. In total, fossil fuel subsidies were still around six times those available to renewables. India highlights the challenges of achieving both rapid economic development and greater environmental and climate sustainability, when cheap and viable renewable energy options are still in their infancy.

Additionally, many of the central government’s post-2020 targets are not yet backed up by binding legislation. These include the 40% renewable energy by 2030 and an E-mobility plan which requires only electric vehicles to be sold by 2030. Environmental policy in India is generally poorly implemented or enforced, and data on compliance tests are often unavailable or access is restricted. Overlapping but different regulations is likely to give rise to inefficiencies, and this makes it more difficult to navigate through the system.

India does have a de facto carbon tax on coal, which was introduced in the 2010 Finance Act. The rate of the ‘cess’ has increased eight times since 2010, reaching INR 400/t (USD $3.2/t) of coal. However, the rate is not yet high enough to have significantly discouraged the use of coal.

Large regional disparities in economic development and voter priorities further dilute initiatives implemented at the national level. The top ten performing states on constraining emissions are generally those that have the highest per capita income, that rely more on renewables, and that have more forest cover. In contrast, tackling climate change is a low priority in the poorest states, where basic necessities are hard to come by for many citizens. The upshot is that environmental policy varies greatly across regions, with the enforcement of the laws and regulations that do exist hampered by a lack of coordination, skills gaps and financial constraints.

Although India is a stable democracy, corruption is widespread throughout the government. This is reflected in the ASI Political and Governance index, where India ranks 75th in our Transparent Laws indicator and 61st in our Absence of Corruption indicator (out of 135 countries) (see Chart 20). Some of the issues include lack of transparent bureaucracy and bribery also permeates India’s private sector. However, it has been improving: India has risen 23 points in the World Bank’s Ease of Doing Business index, and is now in 77th place.

Chart 20: Improvement needed on Political and Governance

Corporate incentives and real time challenges from climate change are building momentum

On the corporate side, informal or industry group lobbying by businesses to loosen environmental policies occurs, although it is less widespread than in other major emerging markets. Many Indian companies are already feeling the physical effects of climate change and are not waiting for the government to legislate or resolve organisational and funding issues before taking action. Utilities companies have actually been lobbying for incentives to help curb emissions to meet rules to reduce emissions that cause pollution, disease, and acid rain.

Schemes such as Perform, Achieve and Trade (PAT) help facilitate the industrial sector’s transition to consume less energy; the first cycle, from 2011-2014, overachieved targets. However, there is room for improvement with regards to transparency in the regulations and mechanisms. In the steel sector, energy efficiency has been promoted through the UNDP project Energy Efficiency in Steel Re-rolling Mills (2004-2013) by aiding low carbon technologies. Meanwhile, state-owned India Railway Finance Corporation has started issuing green bonds to attract new investors.

On the other hand, power companies (DISCOMs)’, have been struggling to pay back their debts to the banks due to poor sales and mandated fixed costs to thermal power developers. These fixed costs are not conducive to power companies signing more purchasing power agreements with renewables suppliers, for example. The UDAY (Ujwal DISCOM Assurance Yojana) scheme was launched by Modi to help these DISCOMs with their finances. However, it has had questionable results. State governments have taken on 75% of the debts, and this has had a harsh effect on state finances.

Case Study 3: China Climate Policy Assessment

China’s Communist party-led system means that the government’s decision to tackle climate change was rolled out with less challenge than in open market, democratic societies

China’s centralised Communist party-led system can be seen as an advantage in trying to address climate change. Party policy divergences and electoral cycles are not a constraint on action. And thus at a time when CO2 mitigation is viewed as a real time crisis because of the link between emissions, pollution and lower life expectancy, policy and actions can change very quickly.

The same is true of the country’s economic structure. The dominance of industry makes it more challenging to address climate change, particularly when activity continues to grow well above the global average. However, the fact that many of the largest polluters are state-owned does make it easier for the government to direct and enforce changes in energy and emissions intensity when it chooses to do so.

One of the major changes to environmental policy in recent years was the centralisation of responsibility for climate issues to the new Ministry of Ecology and Environment (MEE). This created a single supervisory role for CO2 emissions regulation, as well as regulations for water, agricultural pollution and marine conservation. The coordination of environment and climate regulation has therefore improved and simplified, while red tape has been removed.

However, the system and size of China also creates some challenges in terms of local transparency and provincial characteristics

While climate policy regulation is mostly centralised, local authorities do play a role in approving energy projects and implementing legislation. Provinces also face quite different constraints and challenges in terms of how the population is distributed, weather patterns and economic structure. For example, in Shanghai, where population density is more than 900 people per square km and the living standards are high, mass public transportation is more viable than in the western province of Xinjang, where population density is between 0 and 50 people per square km.

Chart 21: Coal remains 60% of Chinese emissions

Renewable energy has accelerated from a very low base thanks to extensive policy action on energy producers and key sectors like autos; however, backsliding is a risk.

In spite of the high level of coal use, renewable energy is a significant growth market in China. Hydroelectric power accounted for 8% of energy consumption in 2017, up 506% since 1995, though storage problems are constraining further growth. And while other renewables only accounted for 3% of energy use in 2017, they have grown over 1000% since 1995, albeit from a low base. BP forecasts suggests this will continue to grow but at a slower pace, with renewables expected to comprise 18% of total energy use in China by 2040.

This mostly reflects the concerted policy effort by the Chinese government to subsidise green energy projects. Indeed, a recent study by Yan et al. at Royal Institute of Technology found that solar power is now less expensive than grid electricity in every Chinese city and solar energy firms have become profitable even without government subsidies. In the auto sector, a significant incentive scheme for consumers to purchase electric cars is supporting companies. Within petrol/diesel vehicles, government regulations have forced distributors to upgrade the emission standards for the cars they sell.

Beyond subsidies and command and control regulations, the national CO2 emissions trading scheme was launched at the end of 2017, building on earlier pilot programmes in major Chinese cities. Local systems had been vastly different to the national scheme in terms of coverage, allowance allocation and penalties for non-compliance.

The national trading programme has three phases:

Phase 1 (2018) Take approximately one year to establish unified national systems for emissions data reporting, registration and allowance trading

Phase 2 (2019) Take approximately one year to conduct mock trading of allowances in the power generation sector

Phase 3 (2020) Conduct spot trading of allowances among participants from the power generation sector. Once the carbon market for the power generation sector is successfully established, the market shall gradually expand to cover other sectors, trading products and trading types.

This plan currently explicitly covers power generation larger than 26,000 tons of CO2 per year, which would cover around one third of total CO2 emissions in China. However, it is intended to eventually cover steel and iron, non-ferrous metals, building materials, chemical industry, petrochemical industry, paper making and civil aviation. The Ministry of Ecology and Environment can impose penalties on entities for non-compliance. While no official targets are available, the Chinese government promotes this programme as a key part of its plan to reduce emissions intensity by 60-65% in 2030 relative to 2005.

However, Chinese climate policy is by no means perfect. Its Nationally Determined Contributions target has been criticised for not being sufficiently ambitious for China to undertake its share of the abatement necessary to limit warming to below two degrees Celsius. And though the single party political system presents some advantages, it also has disadvantages, including low transparency and high corruption, with China ranking 104th of 135 countries for transparent laws and 76th for corruption.

Meanwhile, the ability of policy priorities to change quickly is a double-edged sword, as climate change mitigation could be relegated to a low policy priority at any time, particularly when air quality improves. Signs of this have been seen recently as new coal capacity has been allowed in some provinces in the wake of slower economic growth, while the growth rate of new installed renewable capacity has fallen away significantly.

More generally, although the regulatory environment and commitment to green the domestic economy continues to strengthen in key sectors like autos where producers are required to stock increasing numbers of electric cars, the national policy environment for energy is changing around the margins as China attempts to switch from scale to quality in renewable projects.

For investors, the Chinese market is opening up including a nascent green bond market, but transparency and access can still be challenging

Chart 22: Chinese green bonds growing from non-existent base

Historically, China has been a very difficult economy for foreign investors to access due to severe restrictions on what foreigners can invest in, how that investment can take place, and their ability to repatriate their capital when circumstances require it. In the past few years, however, China’s foreign investment regime has become less restrictive.

Chinese capital markets have become more open; caps on foreign investment have been relaxed; investor eligibility and channels into the bond market have increased; and the stock connect with Hong Kong allows investors with accounts in both onshore and offshore accounts to trade equities between the two markets. However, in the renewable space the market is very much still in its infancy, with no onshore renewables investment incentive schemes available. Corporate green bond issuance overseas is growing, but it remains low relative to other major markets.

Transparency in company accounting also remains problematic. Credit ratings are often done locally; trading is limited in terms of frequency and number of firms open to be traded; and equity derivatives trading is not possible for investors unless linked specifically to a local partner. For more details, see the China local equity market primer on aberdeenstandard.com.

The EU’s large surface area means that countries face quite different climate, demographic and economic constraints that drive differing performance in terms of emissions

Chart 23: EU energy mix relies on fossil fuels

The EU’s economic development path, weather patterns and energy endowment have had important implications for the development of its physical infrastructure, its energy mix, and hence its greenhouse gas emissions. In relative terms, the European economy and thus energy demand grew rapidly after the Second World War until the global financial crisis. Many countries also have both hot summers and cold winters, generating demand for temperature regulation for large parts of the year. With the high relative cost of renewable energy until very recently, and the EU’s own fossil fuel endowment comparatively low, the EU became heavily reliant on imported fossil fuels to satisfy its growing energy demand.

While the EU’s current energy mix remains heavily reliant on fossil fuels (see Chart 23) there is significant variation across member states. For example, over 50% of Sweden’s energy consumption in 2017 came from renewable sources. The renewable energy share was above 30% in Finland, Latvia, Denmark and Austria (see Chart 23). In contrast, the renewable energy share was below 10% in Luxembourg, the Netherlands, Malta, Belgium and Cyprus. The relative use of nuclear energy (high in France), natural gas (high in Germany) and coal (high in Poland) also varies significantly. Emissions profiles and abatement costs and opportunities also necessarily vary a great deal.

Chart 24: EU slow and steady path to sustainability

Nevertheless, even the countries with the lowest shares of low carbon energy have much lower emissions intensity than the United States average. This partly reflects its economic structure (mining and smelting activity is relatively low), and partly its demography (high population density results in lower average housing footprints and widespread mass transit systems), but also its historic policy choices. Indeed, Europe is unique in terms of the vote share of Green parties, and perhaps more importantly, in how little partisan conflict there is over climate goals.

What holds of the average does not apply to each country identically and at all times. France is an interesting case in point. Though the country has very ambitious renewable energy targets and its high use of nuclear energy makes it a comparatively light user of fossil fuels, the government’s attempt to impose an additional carbon tax was the catalyst for the gilets jaunes mass protests. Though the protests reflected wider discontent about the state of the post-global financial crisis French economy and society, they demonstrate how easily support for environmentally focused policies can fracture when living standards are under pressure and the direct costs of action are perceived to be high.

The climate policy environment in the EU is comparatively very strong with the world’s first and largest emissions trading scheme